Quick Summary

2026 Update: Loans for single moms are more accessible than most people realise. Whether you need government house loans for single moms with zero down, student loans for single moms going back to school, or emergency funds for an unexpected bill, there are real programs available right now. This guide covers every major loan type so you can find what fits your situation and move forward.

Being a single mom means you carry the entire financial picture on your own — and when something goes wrong, there’s no one to share that weight with. Financial loans for single mothers in 2026 cover far more ground than most people realise. Some have flexible credit requirements. Some are government-backed with rates banks can’t match. A few don’t require repayment at all.

Min Down Payment

FHA Home Loans

Max SBA

Microloan Amount

Down Payment

USDA Rural Loans

Approval Speed

Emergency Loans

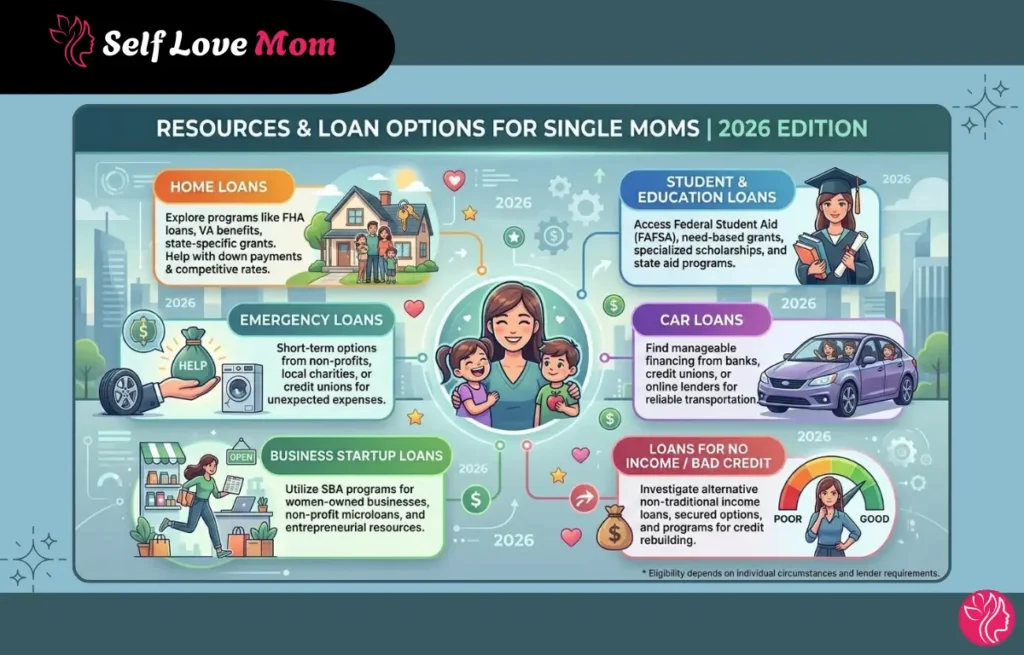

What Types of Loans Are Available for Single Moms in 2026?

Before you start searching, it helps to know which category matches your situation — because each one works completely differently:

- Home loans for single moms — mortgage programs and first-time buyer grants

- Student and Education Loans— for moms in college or going back to school

- Emergency loans — fast help for unexpected expenses

- Car loans — including options for bad credit

- Business Loans — for moms building their own income

- Personal loans for single moms — for general financial gaps

- No income programs — when standard lending isn’t an option

Home Loans for Single Moms

Whether you’re looking at first time home buyer loans for single moms or comparing mortgage loans for single moms based on your credit score, there are solid federal programs available in 2026. State housing agencies also offer home loan grants for single moms that stack on top — money you never pay back.

Here are some of the best options for house loans for single moms in 2026:

The most popular path for first-time buyers. Just 3.5% down with a 580 credit score — and even a score in the 500s may qualify with 10% down. One of the most realistic loans for single moms to buy a house when you’re rebuilding credit.

If you served in the military, this is hands-down the best deal going. Zero down, no private mortgage insurance, and competitive rates. Apply through a VA-approved lender or at va.gov.

Zero down payment for rural and suburban areas. These are true government house loans for single moms — income limits apply, but are higher than most people expect, so check even if you live near a city. No PMI required.

Only 3% down with lower mortgage insurance costs. One unique feature: it counts income from a roommate or family member living with you, which is a real help in multigenerational households.

Also, 3% down with flexible credit requirements. Allows a non-occupying co-borrower if a family member wants to support your application without living in the home.

Free counselling from HUD-approved agencies to help you find down payment grants, understand your loan options, and review your credit before you apply. One of the most underused resources for loans for single moms to buy a house.

Student and Education Loans for Single Moms

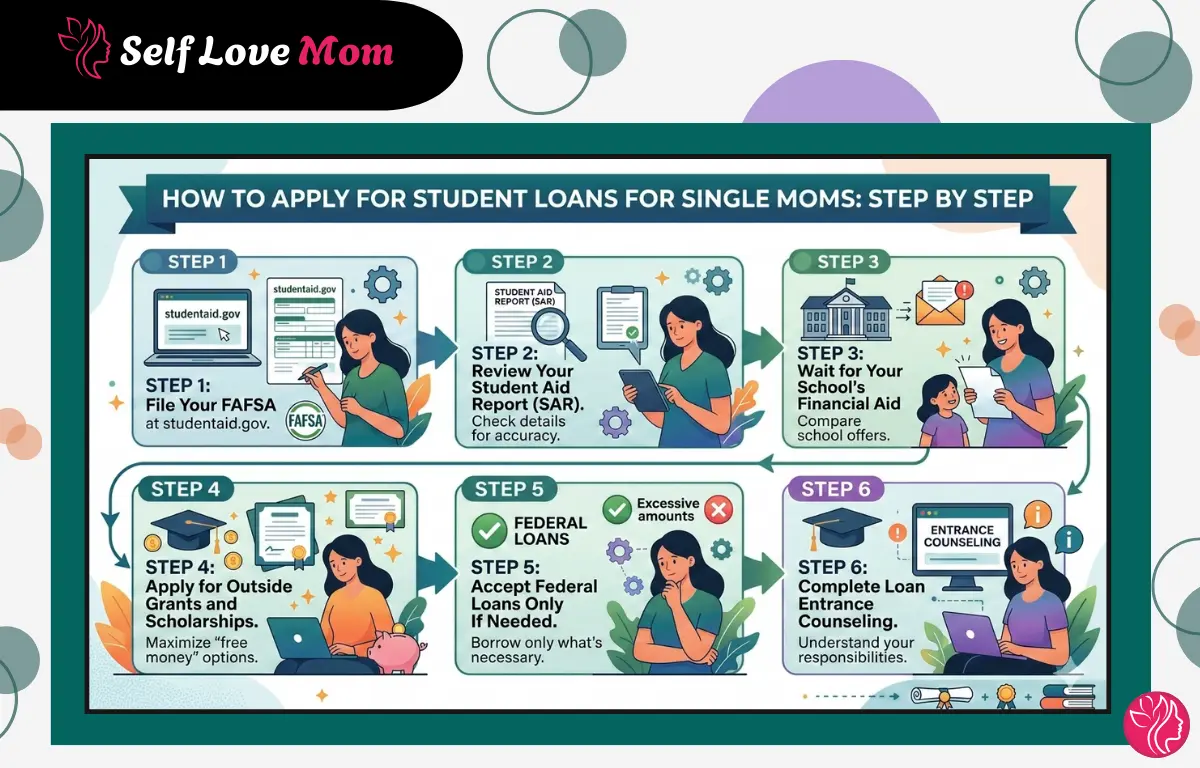

Going back to school is often the move that changes everything long-term — it’s the one investment that raises your income ceiling for good. The good news: student loans for single moms in 2026 are more accessible than they’ve ever been, especially once you understand how independent student status works in your favour.

Start with FAFSA — Every Time

Before you look at any private lender, file the FAFSA. As a single parent, the government classifies you as an independent student, which means more aid is calculated on your income alone. Here’s what that opens up:

- Higher Pell Grant amounts — free money that’s never repaid

- Subsidised Direct Loans, where the government covers interest while you’re in school

- Income-driven repayment so monthly payments actually match what you earn

- A path to Public Service Loan Forgiveness for healthcare, education, and nonprofit work

Here are the best programs for loans for single moms going back to school in 2026:

Up to $7,395 per year for 2025–26 — never repaid. Most single moms with low to moderate income qualify. Always the first step before any loans for single moms in college.

The best of the loans for single moms in school. Interest doesn’t build while you’re enrolled at least half-time. The 2025–26 rate is 6.53% for undergrad borrowers — far below most private lenders.

Caps payments at 5% of your discretionary income. If income is low enough, your payment can literally be $0/month while still counting toward forgiveness after 10 to 25 years.

Active in multiple states with grant money and low-interest support for single parents pursuing degrees or vocational training. Search your state’s chapter for deadlines and requirements.

Cash grants for women who are their family’s main financial provider and are using education to build a better future. No repayment — apply alongside your federal aid, not instead of it.

Covers tuition, books, childcare, and transportation for low-income moms in career-focused programs. Not a loan at all — contact your local American Job Centre to check what you qualify for.

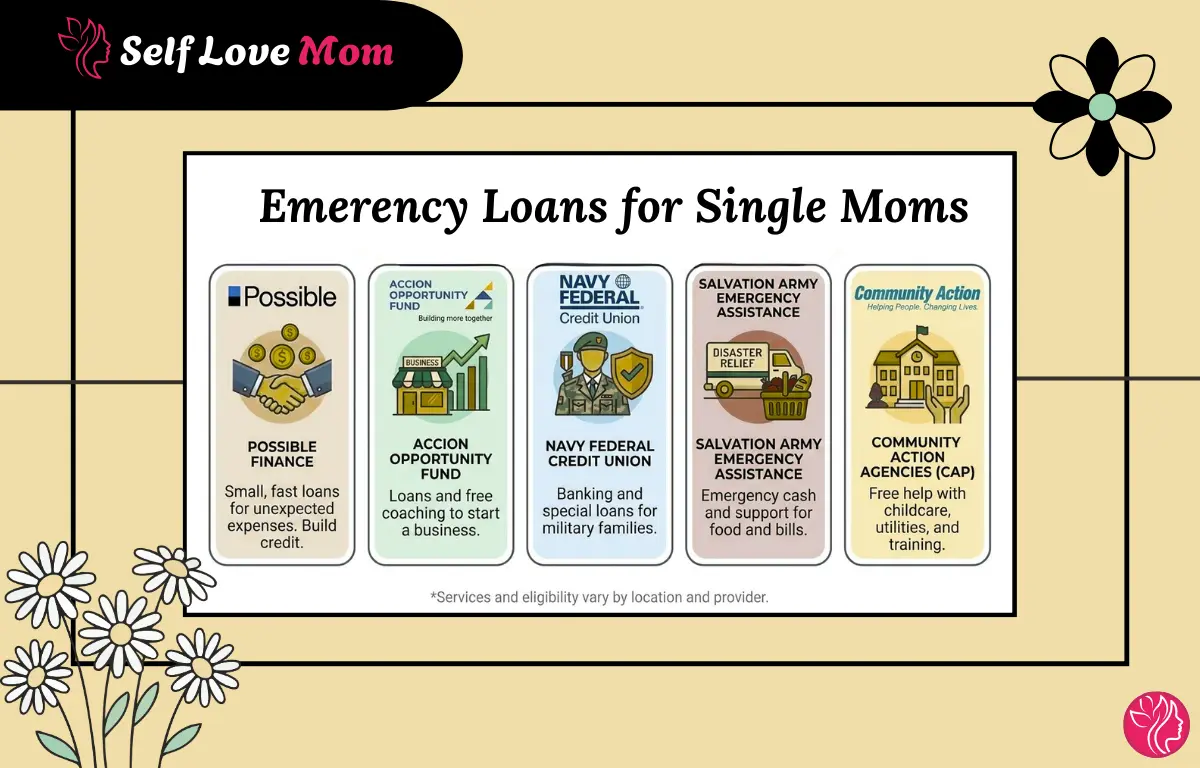

Emergency Loans for Single Moms

An unexpected expense when you’re the only income earner can throw your entire budget off in days. Emergency loans for single moms don’t have to mean payday lenders — credit unions, nonprofits, and community organisations all have options that don’t need perfect credit or a lengthy process.

Here are some of the best emergency options avalable right now:

Instalment loans up to $500 with no credit check and app-based approval in minutes. Reports to all three credit bureaus, so every payment builds your score — far safer than a payday loan.

Personal and small business loans from $300 upward, with no minimum credit score for smaller amounts, plus free financial coaching alongside the loan.

Personal loans from $250 to $50,000 with same-day approval at rates that beat most commercial banks. Open to military families, veterans, DoD employees, and their relatives.

Covers rent, utilities, and food directly with no repayment required. Frees up whatever you do have for other pressing needs. Apply at your local branch or online.

Federally funded local agencies offering emergency help for rent, utilities, and food with very few eligibility requirements beyond income. Most counties have one — find yours at communityactionpartnership.com.

Loans for Single Moms with Bad Credit or No Income

Here’s something most people don’t hear until after a rejection: a bad credit score doesn’t automatically mean no. Most single moms who got turned down by a bank just went to the wrong place first. Big banks are selective. But there’s a whole other world of lenders who look at your full picture, not just three digits on a report.

What to Try When Your Credit Score Is Low

If you’ve been declined before, or you already know your score is rough, start here before you give up on loans for single moms with bad credit:

Member-owned, not profit-driven. Many have “fresh start” programs built specifically for people rebuilding credit. Walk in, explain your situation, and actually talk to a person.

If you have a car or even a small savings account, you can use it as collateral to get approved. The lender takes on less risk, so they’re more willing to say yes.

These nonprofits exist to lend to people banks ignore. They care about your circumstances, your character, and your ability to repay — not a credit algorithm.

Sites like LendingClub connect you directly with individual investors. Requirements are often softer than traditional banks, and interest rates can be surprisingly fair for financial loans for single mothers with imperfect credit.

Got a sibling, parent, or close friend with decent credit? Ask them to co-sign. Your rates drop and approval odds jump significantly.

Loans for Single Moms with No Income

This is trickier, but not impossible. If you’re between jobs, on leave, or living off benefits right now, you still have options — they’re just not at your local bank branch.

- Child support, alimony, SNAP, TANF, and SSI payments legally count as income on most applications. List them — all of them.

- Local nonprofits and Community Action Agencies often have emergency funds that don’t require a pay stub at all.

- Certain states run interest-free micro-loan programs through social service offices — worth a phone call to your county to find out.

Car Loans for Single Moms

Your car isn’t optional — it’s how your whole day functions. Car loans for single moms are available through dealerships, banks, credit unions, and online lenders. For car loans for single moms with bad credit, get pre-approved before setting foot in a dealership. That one step tells you your rate upfront and removes the pressure from the financing conversation.

Here are the best car loan options for single moms in 2026:

Pre-approval with no credit score impact, accepting scores from 500. Large dealer network nationwide — a solid first stop for car loans for single moms with bad credit.

Best rates for moms with 660+ credit. Funds go straight to your bank account so you shop as a cash buyer at any dealer — no fees, no down payment required.

Rates from 4.54% APR with 100% financing for qualified members. Open to military families, veterans, and DoD employees and their relatives.

Shows multiple lender offers with one application. Accepts scores from 575 and covers new and used vehicles — good for comparing options side by side without filling out a dozen separate forms.

In-house financing with flexible credit requirements and fixed, no-haggle pricing. Pre-qualify online before visiting — far less stressful than a traditional dealership experience.

Loans for Single Moms to Start a Business

When you’re doing everything yourself, building your own business stops being a dream and starts being a real strategy — your schedule, your rates, your rules. Loans for single moms to start a business have gotten much more accessible through federal programs, nonprofit lenders, and even zero-interest options. Check what grants are available in your state first, because that’s money you never have to pay back.

Here are the best business loan options for single moms in 2026:

Loans up to $50,000 for small businesses and startups, averaging around $13,000. Most SBA intermediaries include free business training and mentoring alongside the funding.

Zero-interest microloans from $1,000 to $15,000 — no credit score required, no interest, no fees. One of the only truly free loans for single moms starting a business. Takes about 30 days from start to funding.

Business loans from $2,000 for women below the federal poverty line with no credit history required. Operates in 14 US cities with financial education included.

Business loans from $5,000 to $250,000 for women-owned and minority-owned businesses. Accepts credit scores from 575 with free coaching included.

Up to $5 million with repayment terms up to 25 years. Best for single moms who’ve been running a business for a year or two and need larger capital to grow. Interest rates are capped and lower than most private business loans.

How to Apply for Loans as a Single Mom

Whatever loan type you’re going for, doing this in the right order saves time, protects your credit score, and gets you better offers:

1

Pull your free report at AnnualCreditReport.com before any lender does. Dispute errors right away — even one removed mistake can raise your score 20 to 30 points and change the rates you’re offered.

2

Buying a house? Start with FHA or USDA. Going back to school? FAFSA before anything else. Starting a business? Kiva or SBA Microloan. Emergency? Credit union or CDFI first. Applying for the wrong type wastes time and can hurt your score.

3

Most lenders need two years of tax returns, two months of bank statements, recent pay stubs, and proof of any benefits or child support. Having these ready before you start speeds everything up.

4

Most lenders offer a soft-pull pre-qualification that shows your likely rate without affecting your score. Use this to compare at least three offers before deciding — multiple hard inquiries can temporarily drop your score.

5

Child support, TANF, freelance work, part-time income, rental income, and side gigs all count. Lenders can only evaluate what you tell them. Many single moms underreport income and get lower offers than they actually qualify for.

6

Before accepting any loan, ask about deferment options, income-based repayment, and hardship programs. Knowing what flexibility exists before you borrow means you won’t be caught off guard if your income changes.

Eligibility Requirements for Every Loan Type

Knowing a program exists is only half of it. Knowing whether you actually qualify before you apply saves you time and a hard credit pull. Here’s what each loan type actually requires:

Home Loan Eligibility

| Loan Type | Min Credit Score | Down Payment | Key Requirement |

| FHA Loan | 580 (500 with 10% down) | 3.5% | Primary residence, mortgage insurance required |

| USDA Loan | 640 recommended | 0% | Eligible rural or suburban area |

| VA Loan | No minimum (620+ preferred) | 0% | Veteran or surviving spouse |

| HomeReady | 620 | 3% | Income at or below 80% of area median |

| Home Possible | 660 | 3% | Income limits apply, primary residence |

Personal and Emergency Loan Eligibility

| Lender | Min Credit Score | Income Required | Approval Speed |

| Upstart | 300+ | Yes (any source) | Same day |

| OneMain Financial | No minimum | Yes | Same day in-branch |

| Avant | 580+ | Yes | Next business day |

| Possible Finance | No credit check | Not required | Minutes via app |

| Accion (CDFI) | No minimum | Not required for small amounts | Varies |

Car Loan Eligibility

| Lender | Min Credit Score | Best For | Down Payment |

| Capital One Auto | 500+ | Bad credit, pre-approval | Varies |

| LightStream | 660+ | Good credit, lowest rates | None required |

| Navy Federal | No minimum stated | Military families, lowest APR | None for qualified |

| myAutoloan | 575+ | Comparing multiple offers | Varies by lender |

Business Loan Eligibility

| Program | Min Credit Score | Time in Business | Max Amount |

| SBA Microloan | No minimum | Startups eligible | $50,000 |

| Kiva US | No credit check | Startups eligible | $15,000 (0% interest) |

| Grameen America | No credit check | No requirement | Starts at $2,000 |

| Accion Opportunity Fund | 575+ | Some history preferred | $250,000 |

| SBA 7(a) Loan | 650+ | 1 to 2 years preferred | $5 million |

You Deserve a Financial Leg Up

The programs in this guide are real — and they’re running right now in 2026. Start with federal and government options, exhaust nonprofit lenders before touching anything high-interest, and call your state housing or education agency directly. Most people leave money behind simply because they didn’t know to ask. You know now.

Frequently Asked Questions

What are the best loans for single moms with bad credit?

FHA home loans, Upstart, OneMain Financial, and credit union credit-builder programs are the most accessible options. CDFI lenders are also worth checking locally since they look at your full financial picture, not just a score.

Are there government house loans for single moms with no down payment?

Yes. USDA loans offer zero down for eligible rural and suburban homes, and VA loans do the same for veterans and surviving spouses. Both are active government house loans for single moms in 2026 with no PMI required.

Can I get emergency loans for single moms with no job?

Standard lenders will likely say no, but Modest Needs Foundation, Community Action Agencies, and 211 connect you to emergency grants that require no employment and no repayment.

Are there free loans for single moms?

Kiva US offers zero-interest microloans for small businesses — these are genuinely free loans for single moms with no fees and no interest. For personal needs, grants through Modest Needs or state emergency assistance are even better since there’s no repayment at all.

Where do I start with home loan grants for single moms?

Start with HUD’s website and your state housing finance agency. Most states run down payment assistance programs that stack on top of FHA or USDA loans. A HUD-approved housing counselor can identify which grants you qualify for at no cost.

Sources

- U.S. Department of Housing and Urban Development (HUD) — FHA Loan Information

- USDA Rural Development — Single Family Housing Guaranteed Loan Program

- Federal Student Aid (studentaid.gov) — Pell Grant and Federal Loan Programs

- U.S. Small Business Administration — Microloan Program

- U.S. Department of Health and Human Services — TANF Program Overview

- Consumer Financial Protection Bureau (CFPB) — Home Buying Resources