Quick Summary

2026 Update: Student loans for single moms are more accessible than most people think, and there’s far more free money out there than anyone actually tells you. Whether you’re starting school for the first time, going back to finish what life interrupted, or already dealing with loan debt, this guide covers every real option available right now. Grants first, federal loans second, private loans only if you genuinely need them.

Going back to school as a single parent involves more than tuition — childcare, income gaps, and timing all factor in. What most single moms don’t realize until later is that the federal aid system is actually designed to work in their favor. Education loans for single moms, single mother student loans, grant programs, forgiveness paths — your situation qualifies for support that standard applicants simply don’t have access to.

Max Pell Grant

Per Year 2025-26

Interest on Subsidized

Loans While in School

Max SAVE Plan

Payment of Income

To Full Forgiveness

Under PSLF

What Kind of Student Loan Help Is Available for Single Moms?

The loan options available span several different categories, and each one works differently. Knowing which applies to your situation will save significant time:

- Federal grants like the Pell Grant that never need to be repaid

- Federal student loans for single parents with fixed rates and income-based repayment

- Student loan forgiveness for single moms through PSLF and Teacher Loan Forgiveness

- Student loan repayment help for single moms through income-driven plans tied to what you earn

- Private student loans for single moms to fill the gap when federal aid isn’t enough

- Single mom grants for student loans through nonprofits, state programs, and campus funds

Start Here: FAFSA and Federal Aid for Single Moms

Before approaching any lender or comparison site, file the FAFSA. The federal government classifies single parents as independent students, meaning aid is calculated on your income alone. For most single moms, that lower income translates directly into more grant money and better loan access. Here’s what independent student status unlocks when looking for help with student loans for single moms:

- Higher Pell Grant amounts since your financial need is calculated on your income only

- Access to subsidized Direct Loans, where the government pays your interest while you’re enrolled

- Additional unsubsidized loan limits are not available to dependent students

- Eligibility for campus-based aid like SEOG grants and Federal Work-Study

- A path to Public Service Loan Forgiveness if you work in healthcare, education, or a nonprofit

FAFSA opens October 1st. Many aid programs are first-come, first-served. Filing in October versus April can be the difference between a full grant package and getting nothing left.

Federal Student Loan Types and Eligibility

Federal education loans for single moms offer fixed rates, income-based repayment, and forgiveness options — protections private lenders don’t provide. Here’s what’s available for student loans for single moms through the federal system in 2026:

The government pays your interest while you’re in school at least half-time, during the grace period, and during deferment. Best deal available for students with financial needs. No credit check required.

Available regardless of financial need. Interest starts building immediately, but you can defer payments until after graduation. No credit check required, making these accessible for student loans for single moms with bad credit, too.

For graduate programs, PLUS loans cover up to the full cost of attendance. Higher interest rate than Direct Loans, but still more flexible than any private lender with stronger repayment protections built in.

Federal Loan Annual Limits for Independent Students

| Year in School | Subsidized Limit | Total Limit (Sub + Unsub) |

|---|---|---|

| 1st Year | $3,500 | $9,500 |

| 2nd Year | $4,500 | $10,500 |

| 3rd Year and Beyond | $5,500 | $12,500 |

| Graduate | Not eligible | $20,500 |

Grants First: Free Money You Never Repay

Grants are the part of student loans and grants for single moms that most people underestimate. None of it needs to be repaid, and applying for grants before any loan consistently reduces how much you end up borrowing. These are the best student loans for single moms in 2026:

Up to $7,395 per year for 2025-26, completely free and never repaid. Single moms with low income qualify in most cases. Apply through FAFSA at studentaid.gov — this is always the first step before anything else.

An extra $100 to $4,000 per year stacked on top of Pell for students with exceptional financial need. Ask your school’s financial aid office directly — this one rarely gets mentioned upfront.

Cash grants for women who are the primary financial providers for their families. No repayment, ever. Single moms fit the criteria almost exactly and applications open annually.

Active in multiple states, providing grant money and emergency funds specifically for single parents in school. Search for your state’s chapter to find deadlines and eligibility requirements.

For low-income moms in career-focused programs, WIOA can cover tuition, books, childcare, and transportation at no cost. Not a loan at all. Contact your local American Job Center to check what you qualify for.

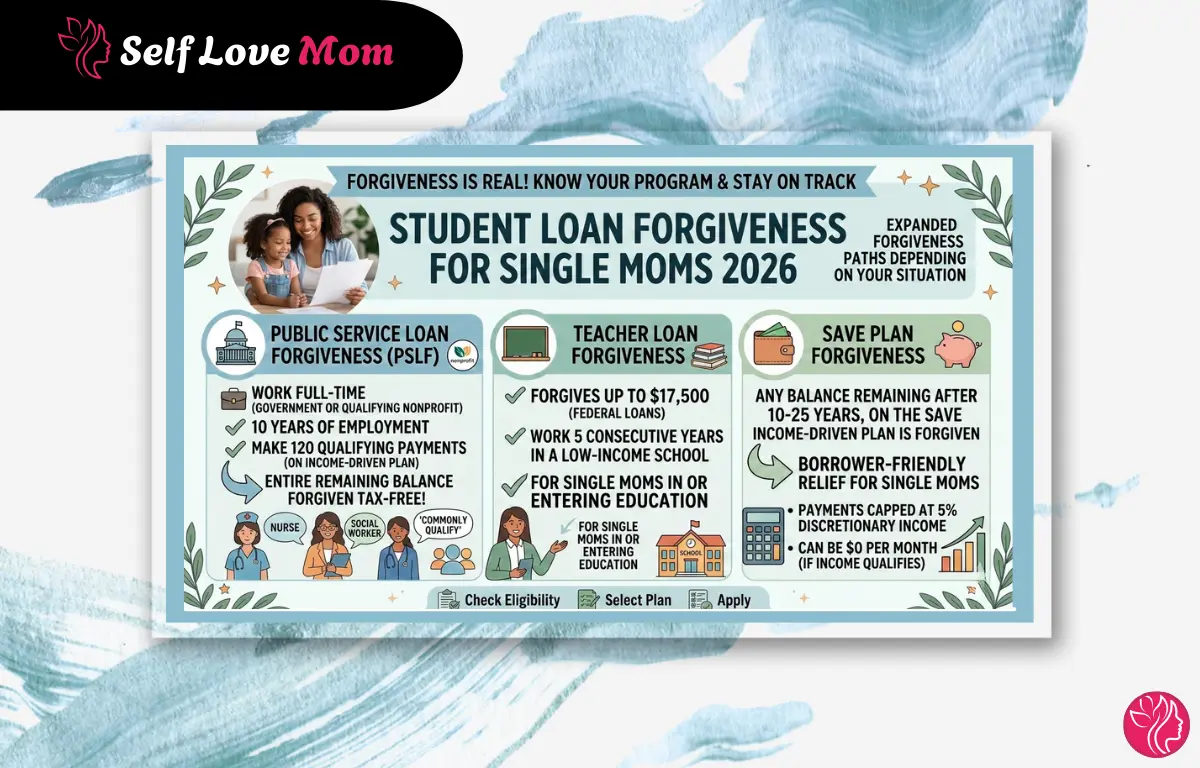

Student Loan Forgiveness for Single Moms

Student loan forgiveness for single moms requires being on the right repayment plan and submitting the correct paperwork each year — it doesn’t happen automatically. For those who qualify, it eliminates balances that would otherwise take decades to clear. Here’s what’s active in 2026:

Work full-time for a government agency or qualifying nonprofit for 10 years while making payments on an income-driven plan, and your entire remaining balance is forgiven tax-free. Nurses, teachers, and social workers commonly qualify.

Forgives up to $17,500 in federal loans for teachers who work five consecutive years in a low-income school. A strong option for single moms in or entering education.

Any balance remaining after 10 to 25 years on the SAVE income-driven plan is forgiven. Payments are capped at 5% of discretionary income and can be $0 per month if your income qualifies. The most borrower-friendly student loan debt relief for single moms is currently available.

Private Student Loans for Single Moms

Private student loans for single moms are worth considering only after federal aid and grants have been exhausted. They cover remaining gaps but come without income-driven repayment, forgiveness options, or the same deferment protections federal loans provide. If you do need one, borrow only what the gap requires and compare multiple lenders before deciding.

Good pick if you need flexible payment options — you can skip one payment per year and adjust your monthly amount as your situation changes. Recommended credit score 650+. Co-signer accepted.

One of the few private lenders that covers part-time students, which matters a lot for single moms who can’t go full-time. No stated minimum credit score. Co-signer option available.

Competitive rates if your credit is in decent shape (670+). You pick your repayment term — 5, 8, 10, or 15 years — so you can keep the monthly payment manageable. Co-signer accepted.

One of the few private lenders that doesn’t require a co-signer. Their outcomes-based loan looks at your school and field of study rather than just your credit score, with a minimum credit score of 540+.

Designed for non-traditional and international students. No credit history or co-signer required — one of the most accessible private loan options for students with limited credit backgrounds.

Student Loans for Single Moms with Bad Credit or No Income

Credit score matters far less than most people assume when it comes to student loans for single moms. Federal Subsidized and Unsubsidized Direct Loans require no credit check for undergrads — eligibility is based on enrollment status and financial need. A lower income actually strengthens your federal application, not weakens it.

If You Have Bad Credit

- Federal Direct Loans require no credit check. Apply through studentaid.gov via FAFSA

- Ascent’s outcomes-based private loan evaluates your school and program, not just your score

- Credit union student loans tend to have more flexible underwriting than big banks

- Adding a co-signer to a private loan can unlock much better rates, even with a weak credit history

If You Have No Income

On the federal side, limited income increases your demonstrated financial need — which means larger grant awards and stronger eligibility for subsidised loans. Private lenders are less flexible; most require a co-signer when income is limited. Sallie Mae is one of the few that factors in projected earnings for students nearing graduation.

Avoid for-profit lender ads that target struggling parents. Some companies market high-interest personal loans disguised as student loans. Legitimate student loans are either through studentaid.gov for federal options or well-known private lenders like those listed in this guide.

Student Loans for Single Moms Eligibility Breakdown by Program

Knowing a program exists is one thing — knowing whether you qualify before applying is more useful. Here is a breakdown of student loans for single moms eligibilty by loan type:

Federal Aid Basic Requirements

- ✓ Be a U.S. citizen, permanent resident, or eligible non-citizen (DACA students currently do not qualify for federal loans)

- ✓ Have a high school diploma, GED, or completed a homeschool program recognized by your state

- ✓ Be enrolled or accepted at an eligible degree or certificate program at least half-time

- ✓ Maintain satisfactory academic progress as defined by your school, usually a 2.0 GPA or above

- ✓ Have a valid Social Security number

- ✗ Cannot be in default on any existing federal student loan. Resolve the default first via rehabilitation or consolidation

- ✗ Cannot owe a refund on any previously received federal grant

Pell Grant Eligibility

| Requirement | Details | Single Mom Advantage |

|---|---|---|

| Financial Need | Based on EFC from FAFSA | Single income = lower EFC = more aid |

| Enrollment | Full or part-time eligible | Part-time counts, good for working moms |

| Degree Level | Undergraduate only | Grad students not eligible |

| Lifetime Limit | 12 semesters (6 years) | Transfer credits count toward limit |

| Prior Degree | Cannot already hold a bachelor’s | 2nd bachelor’s not eligible |

Subsidized Direct Loan Eligibility

| Factor | Requirement | Notes |

|---|---|---|

| Credit Check | None required | Bad credit is OK |

| Income Requirement | Must demonstrate financial need | Low income = easier to qualify |

| Enrollment | At least half-time | Typically, 6 or more credit hours |

| Degree Level | Undergraduate only | Grad students use unsubsidized |

| Interest While in School | The government pays it | Best feature of this loan |

Private Loan Eligibility: What Lenders Look At

| Factor | Typical Requirement | Workaround if You Don’t Qualify |

|---|---|---|

| Credit Score | 640 to 700 minimum for most | Add a co-signer or use Ascent/MPOWER |

| Income | Steady income preferred | Benefits, child support, and part-time work count |

| Enrollment | At least half-time at an eligible school | Some lenders allow less than half-time |

| Citizenship | U.S. citizen or permanent resident | MPOWER serves non-traditional students, too |

| Debt-to-Income | Varies by lender | A co-signer with a lower DTI helps significantly |

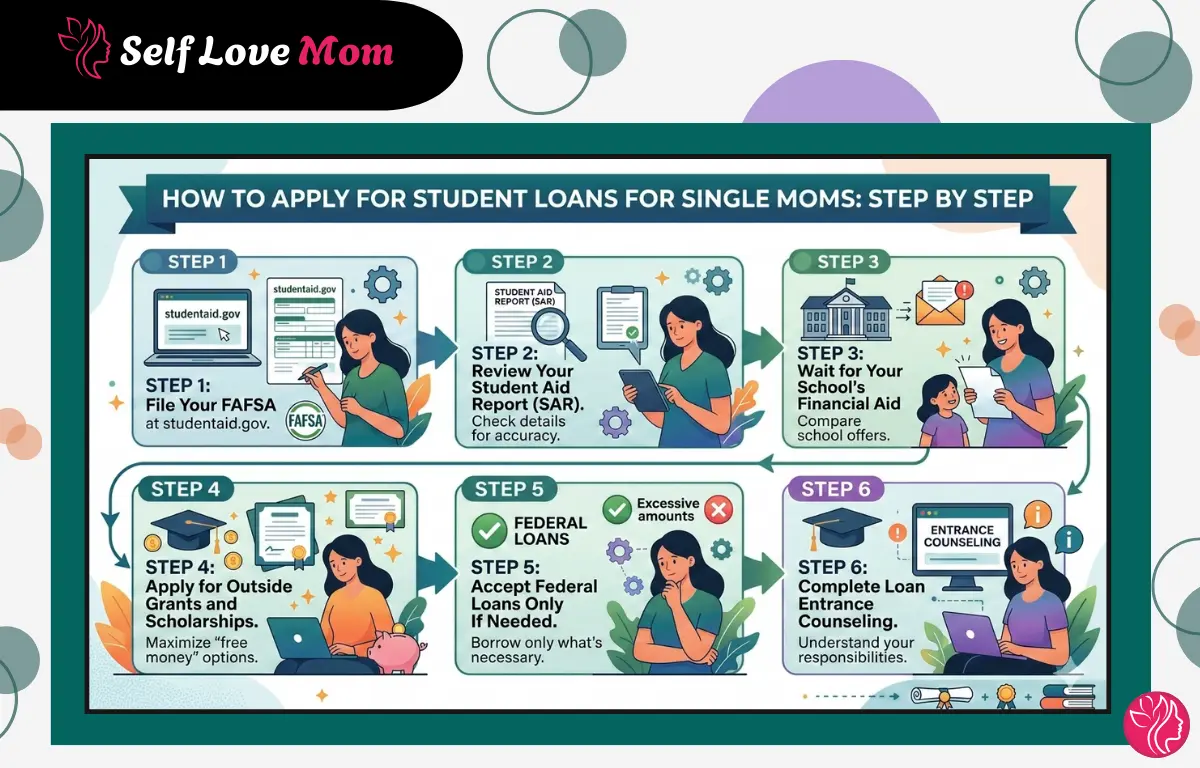

How to Apply for Student Loans for Single Moms: Step by Step

Follow this order to apply for student loans for single moms. Start with free aid, move to federal loans only if a gap remains, and treat private lenders as a last step.

Opens October 1st for the following academic year. Use your most recent tax return. As a single mom, you file independently — your parents’ information is not required. Takes about 30 to 45 minutes.

You’ll get this within days of submitting. Check it for errors right away. Your Expected Family Contribution is listed here — the lower it is, the more aid you qualify for.

Your school uses your SAR to build an aid package with grants, work-study, and loans. You don’t have to accept the loans. Accept the grants first, then decide whether you actually need the loans.

While you wait, apply for Soroptimist, Jeannette Rankin, Patsy Mink, and any state-specific single parent scholarships. These don’t affect your federal aid eligibility and can reduce your borrowing further.

After grants and scholarships, if there’s still a gap, take subsidized loans first and unsubsidized second. Private student loans for single moms are the last resort — not the starting point.

Required before your first federal loan is disbursed. Takes about 20 minutes online at studentaid.gov. It explains your rights and responsibilities as a borrower and is genuinely worth reading.

Real Tips to Get More Aid as a Single Mom

Getting meaningful student loan help for single moms often comes down to knowing what to ask and who to ask it. These are steps most applicants skip — and they consistently make a real difference:

1. Before You Apply

- Call the financial aid office directly and ask: “What additional aid is available for single parents?” Many schools have emergency funds, childcare grants, and institutional scholarships that never get advertised. The financial aid counselor knows about all of them.

- File a Special Circumstances Appeal if your income dropped recently due to job loss, divorce, or reduced hours. You can ask the financial aid office to use your current year income instead of last year’s tax return. This is called a Professional Judgment Review and it can dramatically increase your aid.

- Apply to multiple schools and compare aid packages. The sticker price of tuition is almost never what you actually pay. A more expensive school might offer a much better aid package than a cheaper one.

2. While You’re Enrolled

- Re-file FAFSA every single year. Aid amounts change based on your updated income and the school’s available funds.

- Ask about childcare assistance on campus. Many schools have subsidized programs for student parents that aren’t widely advertised anywhere.

- Look into WIOA funding through your local workforce development board. It can cover tuition, books, childcare, and transportation on top of your existing financial aid.

- Maintain your GPA. Many grants and scholarships require satisfactory academic progress and one bad semester can cost you thousands in aid.

The Right Support Is Available — Start With What’s Free

From student loans for single moms going back to school to student loan repayment help for single moms managing existing debt — the programs in this guide are active and accessible in 2026. Start with FAFSA, prioritize grants before any loan, and contact your financial aid office directly about institution-specific single mom grants for student loans that may not be listed publicly.

FAQs on Student Loans for Single Moms

What are the best student loans for single moms going back to school?

Federal Direct Subsidized Loans are the best student loans for single moms because interest doesn’t accrue while you’re enrolled. Pair them with the Pell Grant through FAFSA to reduce how much you need to borrow.

Is there student loan forgiveness for single moms?

Yes. PSLF clears your balance after 10 years of qualifying public service payments. The SAVE plan forgiveness applies after 10 to 25 years for everyone else, depending on the loan amount.

Can I get student loan debt relief for single moms on existing debt?

Yes. The SAVE plan can drop your payment to $0 at low income. Deferment pauses payments temporarily. If you’re in default, loan rehabilitation restores your good standing.

Are there student loans for single moms with bad credit?

Federal Direct Loans require no credit check at all for undergrads. For private student loans for single moms with bad credit, Ascent and MPOWER are designed for applicants without strong credit histories.

What single mom grants for student loans are available in 2026?

The Pell Grant covers up to $7,395 per year. The Soroptimist Live Your Dream Award and Single Parent Scholarship Fund are also active. None of these needs to be repaid.

What is the best student loan repayment help for single moms?

The SAVE plan is the strongest option right now. Payments are capped at 5% of discretionary income and any remaining balance is forgiven after 10 to 25 years.

Sources

- Federal Student Aid (studentaid.gov) — Pell Grant Program 2025-26

- Federal Student Aid — Public Service Loan Forgiveness Program

- Federal Student Aid — SAVE Repayment Plan

- CareerOneStop (DOL) — WIOA and American Job Centers

- Consumer Financial Protection Bureau — Paying for College Resources

- National Center for Education Statistics — Student Financial Aid Data