Quick Summary

2026 Update: Government-backed mortgage programs, down payment grants, and first time home buyer loans for single moms make homeownership more accessible than most people realize. FHA loans start at 3.5% down. USDA and VA loans require zero down. Most states offer additional single mom home buying assistance that stacks on top. This guide covers every major option for home loans for single mothers in 2026, including programs for bad credit and low income.

Owning a home on a single income feels out of reach until you look at what’s actually available. Loans for single moms for homes exist at the federal, state, and local level — and many stack together. You can qualify for an FHA loan and a state down payment grant at the same time, which is how a lot of single moms close with very little cash out of pocket.

FHA Loans (580+ credit)

USDA and VA Loans

Down Payment Grants

Some FHA Lenders

Yes. Government home loans for single moms use qualification criteria single parents regularly meet — lower down payments, flexible credit standards, and income thresholds designed for one-income households. Programs for single parents buying a home also stack, meaning grants layer on top of loans.

Types of Home Loans for Single Moms

There are several types of home loans for single moms available in 2026. Whether you’re looking for single mom loans for homes with zero down or need flexibility on credit, here’s a breakdown of the most popular and accessible options:

1. FHA Home Loans for Single Moms

FHA home loans for single moms are among the most popular options and for good reason. Backed by the Federal Housing Administration, these loans offer:

- Down payments as low as 3.5% (with a 580+ credit score)

- Down payments of 10% for credit scores between 500 and 579

- More lenient debt-to-income ratio requirements

- Competitive interest rates

FHA loans are often the best home loans for single moms because they’re designed for first-time buyers and those with limited savings. If you’re a first time home buyer with a modest income, an FHA loan should be your first stop.

2. USDA Loans — Zero Down Payment

USDA loans are one of the strongest single parent low income home loans, especially for those living outside major cities. Backed by the U.S. Department of Agriculture, these government home loans for single moms offer:

- Zero down payment required

- Below-market fixed interest rates

- Income limits up to 115% of the area median income

- Available for homes in eligible rural and suburban areas

- No private mortgage insurance (PMI) requirement

If your target location qualifies, this is one of the lowest-cost mortgage programs for single moms available in 2026. Use the USDA eligibility map at eligibility.sc.egov.usda.gov to check your area.

3. VA Loans — For Veteran Single Moms

If you’ve served in the military, VA loans are the best home loans for single moms veterans on the market. These loans come with benefits no other program matches:

- Zero down payment required

- No private mortgage insurance (PMI)

- Lowest interest rates available among all loan types

- No income cap or loan limit for most borrowers

- Available to veterans, active-duty members, and surviving spouses

The VA does not set a minimum credit score, though individual lenders typically want 580 or above. If you qualify, this should be your first option before any other single mom home loan.

4. Conventional Loans with Low Down Payment

Fannie Mae’s HomeReady and Freddie Mac’s Home Possible are conventional home loans for single moms built for low to moderate-income buyers. Key features include:

- Just 3% down payment required

- Rental income and boarder income count toward qualification

- Non-borrower household income can be used to qualify

- Reduced mortgage insurance rates compared to standard conventional loans

- A credit score of 620 or above is required

These are the best conventional mortgage loans for single mothers who need flexibility in how their income is calculated, especially for low income earners who rent out a room or receive income from other household members.

5. State and Local Programs

Most states run their own mortgage programs for single moms through Housing Finance Agencies (HFAs), often with benefits layered on top of federal loans. What these programs typically offer:

- Below-market fixed interest rates

- Built-in down payment assistance or grants

- Forgivable second mortgages for closing costs

- Priority access for first-time buyers and low-income households

- Income and purchase price limits that vary by county

These single parent home loans are funded annually and availability changes throughout the year. Contact your state HFA directly or search “[your state] housing finance agency” to find what’s currently open.

Home Loan Grants for Single Moms

Grants cover down payments and closing costs without repayment. Most home loan grants for single moms are distributed through state housing agencies or federal programs and are designed to layer on top of the loan programs above.

Up to 5% of the loan amount in down payment assistance. Available in most states, it never requires repayment and works alongside FHA and conventional loans. One of the most accessible grants for home loans for single moms in 2026.

Most states run a first time home buyer program with an outright grant or forgivable second mortgage for the down payment. Search your state name plus “housing finance agency first time buyer” to find current funding.

HUD-funded down payment and closing cost assistance distributed through local organizations. A HUD-approved counselor can connect you with what’s active in your county at no cost.

0% interest mortgages for qualifying low-income families. Sweat equity is required, but the terms are unlike anything a traditional lender offers. A strong option for single mom home buying assistance at very limited incomes.

Grants and loans stack. Qualifying for an FHA loan doesn’t stop you from also receiving a state down payment grant. Apply for both and let your lender coordinate — most HFA-approved lenders handle this routinely.

First Time Home Buyer Programs for Single Moms

First time home buyer programs for single moms layer on top of your base loan. You qualify as a first-time buyer even if you’ve owned before — as long as you haven’t owned a primary residence in the past three years. These programs offer some of the most generous benefits available:

Check current federal and state offerings for tax credits available to first-time buyers. Some states offer a credit of up to $2,000 per year on mortgage interest paid — worth verifying with your state HFA before you close.

Most states offer DPA programs exclusively for first-time buyers, including outright grants and low-interest second mortgages. These home loan grants for single moms never need to be repaid when program requirements are met, and they can cover the full down payment in some states.

Free or low-cost homebuyer education through HUD-approved counselors. Completing a HUD-approved course is required by most down payment assistance programs and can also help you qualify for better loan terms. Available online in most states.

MCCs allow first time home buyer loans for single moms to claim a federal tax credit on a portion of mortgage interest paid each year — typically 20 to 25% of annual interest. This reduces your tax bill every year for the life of the loan, not just at closing. Available through most state Housing Finance Agencies.

Contact your state’s Housing Finance Agency for what’s currently funded. Programs open and close throughout the year based on budget cycles.

Home Loans for Single Moms with Bad Credit

Credit score matters, but it’s not the only factor lenders look at. Home loans for single moms with bad credit are accessible through several programs, depending on where your score actually sits.

Credit Score Requirements by Program

| Program | Minimum Score | Down Payment |

|---|---|---|

| FHA Loan | 500 (10% down) / 580 (3.5% down) | 3.5% to 10% |

| USDA Loan | 640 preferred, exceptions exist | 0% |

| VA Loan | No VA minimum (most lenders: 580+) | 0% |

| HomeReady / Home Possible | 620 | 3% |

When Your Score Is Below 580

- Some FHA-approved lenders manually underwrite bad credit home loans for single moms at 500 to 579 when compensating factors are strong — low DTI or documented savings.

- Credit unions and CDFIs sometimes offer home loans for single mothers outside standard scoring models.

- State housing agencies may have their own low income home loans for single mothers with different thresholds.

- 6 to 12 months focused on the specific items dragging your score often moves it enough to qualify. A HUD-approved counselor can map that out at no cost.

- Pull your free credit report at annualcreditreport.com before approaching any lender. Check for errors — one corrected item can move a score by 20 to 40 points.

- Child support, alimony, and benefit payments legally count as income on mortgage applications. List every source.

- Multiple mortgage applications within a 45-day window count as a single credit inquiry — comparison shopping doesn’t hurt your score the way people think it does.

How to Qualify for Single Mom Home Loans

These are the core requirements across most mortgage programs for single moms. Meeting most of them is enough to move forward with at least one program.

- ✓Income Documentation: Pay stubs, two years of tax returns, child support orders, and benefit letters all count. List every source — lenders can only work with what you tell them about.

- ✓Debt-to-Income Ratio (DTI): Most programs want monthly debts at or below 43% of gross income. FHA and some state programs allow up to 50% with compensating factors.

- ✓Credit History: On-time payment record carries more weight than score alone in manual underwriting. Limited credit history is workable through FHA.

- ✓Down Payment Source: Funds must be documented. Family gift funds are acceptable on FHA loans with a signed gift letter. State grant funds never require repayment.

- ✓Primary Residence: Every program here requires the home to be your primary residence, not a rental or secondary property.

- ✓Homebuyer Education: Required by most down payment assistance programs. Free approved courses at hud.gov/counseling.

- ✓Residency Status: Most federal programs require U.S. citizenship or eligible legal residency. Some state programs have additional flexibility.

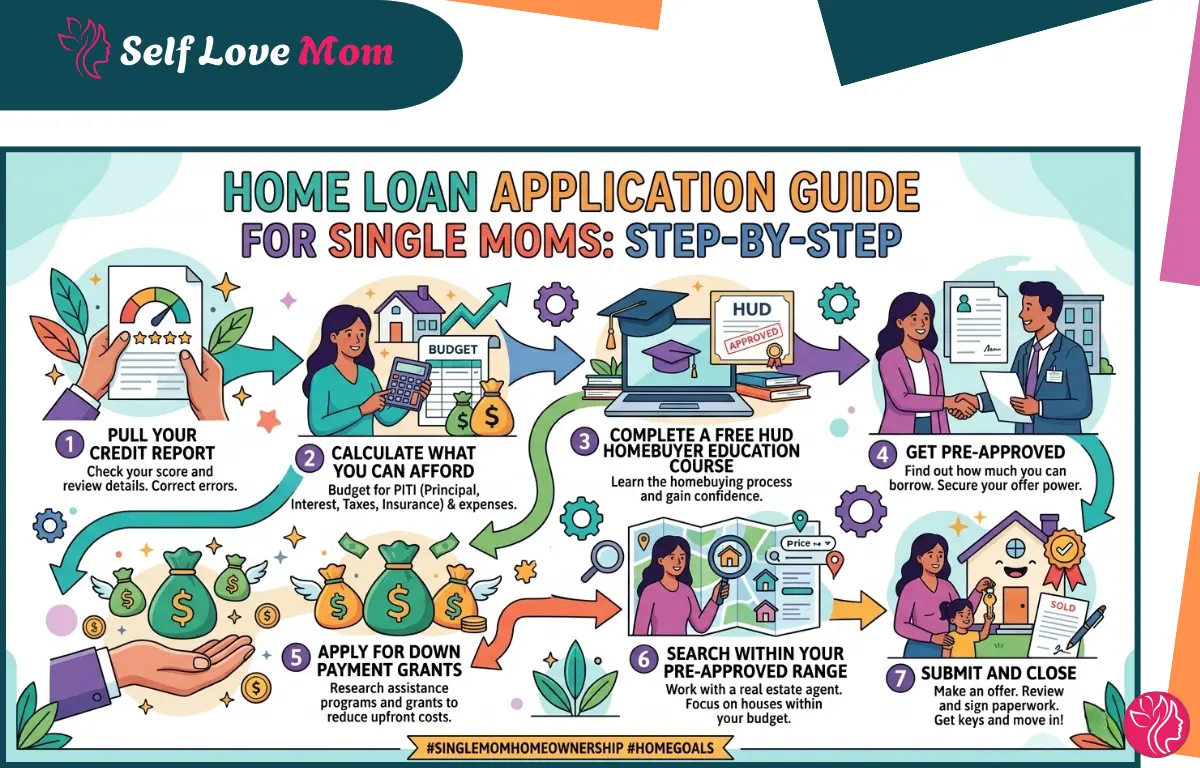

How to Apply for a Home Loan as a Single Mom: Step by Step

Following these steps in order reduces delays and significantly improves your approval odds for home loans for single moms.

Get your free report at annualcreditreport.com. Dispute any errors before a lender sees your file.

Use a mortgage calculator and include property taxes, insurance, and HOA fees — not just principal and interest.

Required by most down payment programs. Find an approved course at hud.gov/counseling — most are free and online.

Choose an FHA, USDA, or VA-approved lender. A pre-approval letter sets your price ceiling and shows sellers you’re ready.

Contact your state Housing Finance Agency. Ask about single mom home buying assistance and any programs for single parents buying a home in your area.

Work with an agent who knows first-time buyer programs. They’ll flag homes that qualify for HUD, USDA, or the grants you’ve applied for.

Your lender handles most of the process. Respond to document requests quickly. Closing typically takes 30 to 45 days from an accepted offer.

FAQs on Home Loans for Single Moms

Are there home loans for single moms?

Yes. FHA, USDA, and VA loans are all actively used as home loans for single moms. Most states also run additional single parent home loans and grant programs that stack on top.

How to buy a house as a single mom?

Check your credit, calculate your budget, then get pre-approved with an FHA-approved lender. Apply for down payment assistance through your state Housing Finance Agency. Complete a free HUD homebuyer education course, work with an agent who knows first-time buyer programs, and stay within your pre-approved range. The full process takes 3 to 6 months from start to closing.

What credit score do I need for a home loan as a single mom?

FHA: 500 with 10% down, 580 with 3.5% down. USDA: 640 preferred. VA: no official minimum (most lenders want 580+). HomeReady and Home Possible: 620.

Can I get a home loan with no down payment as a single mom?

Yes — through USDA loans (rural and suburban areas) and VA loans (veterans and service members). For other loan types, state Housing Finance Agency grants can reduce your out-of-pocket cost to near zero.

Do single moms qualify for first-time homebuyer programs?

Yes, as long as you haven’t owned a primary residence in the past three years. First time home buyer programs for single moms are available at the state level, and the eligibility rules are broader than most people realize.

What documents do I need to apply for home loans for single moms?

Typically: 2 years of tax returns, recent pay stubs, 2–3 months of bank statements, proof of child support or alimony (if applicable), photo ID, and Social Security number. Your lender will provide a full checklist.

The Right Support Is Out There

From government home loans for single moms to first time home buyer programs for single moms — the options in this guide are active in 2026. Start with federal programs, layer on state grants, and let a HUD-approved counselor map out what stacks in your area.

Sources

1. U.S. Department of Housing and Urban Development — FHA Loan Information

2. USDA Rural Development — Single Family Housing Programs

3. U.S. Department of Veterans Affairs — VA Home Loans

4. Fannie Mae — HomeReady Mortgage

5. National Homebuyers Fund — Down Payment Assistance Programs

6. Habitat for Humanity — Homeownership Programs