📋 Quick Summary

2026 Update: Emergency loans for single moms are easier to get than most people assume, and this guide covers every real option available right now. From same-day online lenders to nonprofit grants you never have to pay back, help exists no matter your credit score or employment status. Bad credit, no job, child support as income, it all counts with the right lender.

When you are raising kids on your own, there is no backup plan when a financial emergency hits. The car breaks down, the rent comes due, a medical bill shows up and suddenly the math just does not add up. Emergency loans for single moms exist for exactly these moments, and getting approved is more possible than most people think, even with bad credit, no steady job, or a complicated financial history.

What Are Emergency Loans for Single Moms?

Emergency loans for single moms are short-term financial products built for speed. When savings are not there and a bill cannot wait, they step in to cover the gap. Personal loans from online lenders, payday alternative loans from credit unions, nonprofit grants, even government programs all fall under this category. The key difference from a traditional bank loan is urgency. Here are the most common situations single moms use them for:

- Medical bills or prescriptions that can’t be delayed

- Rent or mortgage coming up short this month

- A car repair needed to keep the job

- A utility shutoff notice with a deadline attached

- Unexpected childcare costs or school fees

Good to know: Your bank isn’t the only source for emergency loans for single moms. Nonprofits, credit unions, and government programs all have options too. Knowing the full range before you apply can save you a significant amount in interest and fees.

Can Single Moms With Bad Credit Get Emergency Loans?

Yes. And honestly, more easily than most people expect. Bad credit emergency loans for single moms are available through online lenders, credit unions, and nonprofits all across the country. A low score matters, but it is rarely the only thing being considered. Most of these lenders care more about whether you can realistically make the payments than what happened to your credit years ago.

Here is what they typically look at:

- Monthly income from any source. Child support, benefits, gig work, and part-time jobs all count

- How consistent your bank deposits have been over the past few months

- Your debt load compared to what you bring in each month

- Whether your income realistically covers the repayment amount

- Employment status. Freelance and side work are accepted by many lenders

A score under 580 is not the same thing as a rejection. With the right lender, emergency loans for single moms with bad credit are very much on the table. Do not count yourself out before you check.

What Credit Score Do You Actually Need?

| Credit Score Range | Approval Likelihood | Best Option |

|---|---|---|

| 720 and Above | Very High | Traditional banks and credit unions |

| 660 to 719 | High | Online personal loan lenders |

| 580 to 659 | Moderate | Subprime lenders and credit unions |

| 500 to 579 | Low to Moderate | CDFIs, payday alternatives, nonprofits |

| Below 500 | Low but Possible | Nonprofit grants, secured loans, assistance programs |

Even at the bottom of that table, emergency loans for single moms are still within reach through lenders built specifically for people in that position. Apply before you assume the answer is no.

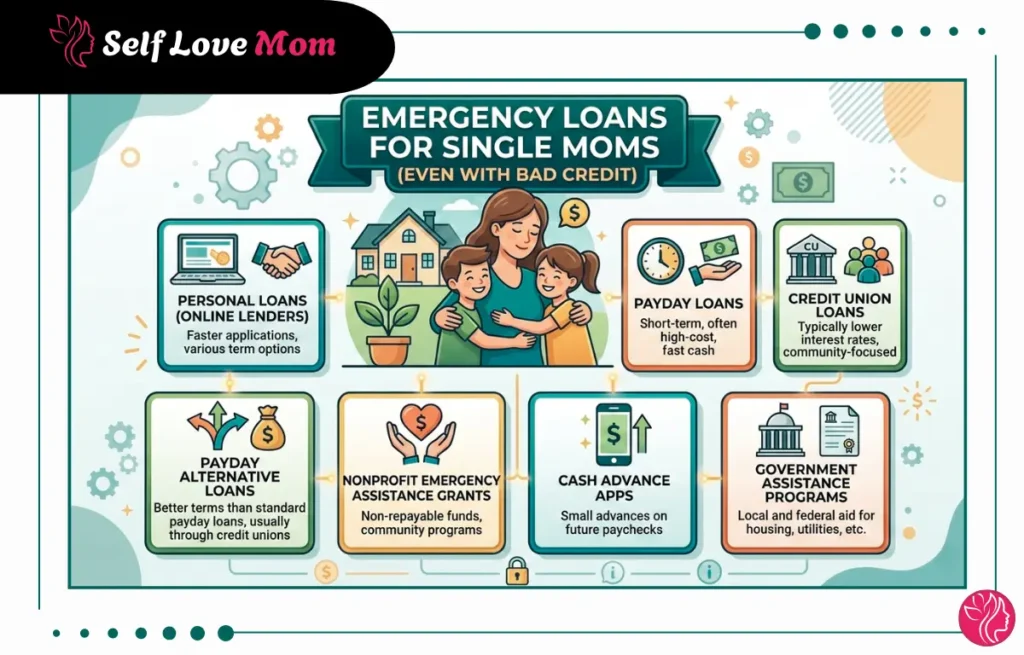

Types of Emergency Loans for Single Moms

Your best option depends on your credit score, income, and how fast you need the money. Some of these require no repayment at all. Others get cash in your account the same day. Here is a breakdown of every type of emergency loans for single moms available right now.

1. Personal Loans (Online Lenders)

Online personal loans are the most flexible option out there. Income and banking history carry more weight than your credit score, which opens the door for applicants a traditional bank would turn away. Funds typically land in your account within one to two business days. Some reputable lenders worth checking first:

- Upstart: accepts credit scores as low as 300, loans from $1,000 to $75,000

- OppLoans: no minimum credit score required, loans from $500 to $5,000

- LendingPoint: works with scores from 600, loans from $2,000 to $36,500

- Avant: accepts scores from 580, loans from $2,000 to $35,000

Fast Funding: Most online lenders deposit funds within 24 to 48 hours of approval. Several offer same-day options when verification is completed early. Prequalification uses a soft credit pull that doesn’t affect your score.

2. Payday Loans

Payday loans give you cash fast, sometimes the same day, with almost no paperwork. That speed is real. But so is the cost. Fees can be steep enough to turn a short-term fix into a long-term problem, so these should be a last resort. The most widely available providers:

- Check Into Cash: one of the largest payday lenders in the country with online and in-store options

- ACE Cash Express: same-day funding online and at thousands of U.S. locations

- Speedy Cash: online application with near-instant approval decisions

- Loan amounts typically between $100 and $1,000

- No credit check required in most cases

💛 Use With Caution: Emergency payday loans for single mothers can carry rates around 399% APR. Use one only when every other option is off the table and you’re certain the full balance can be cleared on your very next payday. Rolling it over is how a small debt quietly becomes a serious one.

3. Credit Union Loans

Credit unions are member-owned, not profit-driven. That difference shows up in lower rates and more willingness to work with people who don’t have a perfect credit history. If you’re already a member somewhere, call them before applying anywhere else. Some well-known options:

- Navy Federal Credit Union: one of the largest in the country, open to military families and extended members

- PenFed Credit Union: personal loans at competitive rates with flexible repayment terms

- Local community credit unions: often the most willing to work directly with your situation

- Personal loans typically from $500 to $10,000 at rates well below traditional banks

Good to Know: Joining a credit union usually requires only a one-time deposit of $5 to $25. That small step can result in meaningful interest savings over the life of any loan.

4. Payday Alternative Loans (PALs)

PALs are the credit union version of a payday loan, federally regulated and far cheaper. The APR is capped at 28% by the National Credit Union Administration. Compare that to the 399% or more that most payday lenders charge and the difference is hard to ignore. Here is what to know before applying:

- Loan amounts from $200 to $2,000 with repayment up to 12 months

- APR capped at 28% by the National Credit Union Administration

- Alliant Credit Union: PALs available to members with competitive terms

- First Tech Federal Credit Union: PAL program available to qualifying members

- Digital Federal Credit Union (DCU): offers PALs nationwide with easy membership

⚠️ Avoid Title Loans: Title loans use your car as collateral, charge APRs that regularly exceed 300%, and give lenders the right to repossess your vehicle if you miss even one payment. For a single mom, that car gets you to work and gets your kids to school. Don’t risk it. Try every other option first.

5. Nonprofit Emergency Assistance Grants

This one’s worth saying clearly: most single moms don’t know these exist. Nonprofit grants require no repayment and don’t touch your credit report. If there’s a chance you qualify, check these before you borrow anything. Organizations that offer direct assistance:

- Catholic Charities: rent, utility, and food assistance with no religious requirement

- The Salvation Army: emergency financial help in nearly every U.S. city

- St. Vincent de Paul: direct help through local councils across the country

- Modest Needs: small online grants for people in short-term financial hardship

- Local Community Action Agencies: emergency cash and vouchers in most U.S. counties

Find Free Help Near YouEnter your zip code at 211.org to see every local grant, emergency fund, and assistance program in your area. Free to use and takes under a minute.

6. Cash Advance Apps

Cash advance apps are a smart middle ground for emergency loans for single moms. They advance part of your next paycheck, pull it back automatically on payday, and charge no interest. No credit check either. For anything under $500, honestly, try one of these before anything else. The most popular options:

- Dave: advances up to $500 with no interest and a small monthly membership fee

- Brigit: advances up to $250 and includes free budgeting tools

- Earnin: access up to $150 per day based on hours already worked

- MoneyLion: advances up to $500 with same-day delivery for members

- Chime SpotMe: fee-free overdraft up to $200 for eligible account holders

How Repayment Works: The advance is pulled back automatically on payday. No rollovers, no late fees, no penalty charges. None of the debt risk that comes with a payday loan.

7. Government Assistance Programs

Before you apply for any emergency loans for single moms, spend five minutes checking what government programs you qualify for. No repayment, no credit check, funded specifically for families in hardship. A lot of single moms are leaving money on the table simply because they didn’t know how to apply. Use our free grants and aid finder to see what you qualify for. Programs worth checking:

- TANF (Temporary Assistance for Needy Families): monthly cash payments for low-income families with children

- LIHEAP: heating, cooling, and electricity bills paid directly to your utility provider

- WIC: food and nutrition support for pregnant moms and children under five

- Emergency Rental Assistance Program (ERAP): up to 18 months of back rent in qualifying states

- SNAP: monthly food benefits that reduce grocery costs and free up cash for other bills

Apply in One Place for emergency loans for single moms. Visit Benefits.gov to see every federal and state program you qualify for based on your income and household size. Free, fast, and could connect you to significant assistance.

How to Apply for Emergency Loans for Single Moms

When money is tight and the clock is running, the last thing you need is a complicated process. Follow these steps to get from application to funded account as quickly as possible.

01

Write down the exact amount you need. The real number for the real expense, nothing rounded up or padded. Borrowing only what covers the emergency keeps repayment realistic from the very first payment.

02

Check your credit score before applying anywhere. Credit Karma and AnnualCreditReport.com are both completely free. Knowing your range means you apply to the right lenders and avoid hard pulls you are unlikely to pass.

03

Gather your documents before you start. You will need a government-issued ID, proof of income, two to three months of bank statements, and your bank details for direct deposit. Having these ready stops the process from stalling at the final step.

04

Compare two or three lenders before committing. Look at the APR, the total repayment cost, and any origination fees. Prequalifying uses a soft pull only and will not affect your score. Upstart and Avant are solid places to start.

05

Complete the application online. Most take under 10 minutes. Upload your documents as you go so nothing holds up the review.

06

Read the full agreement before you sign. Check the APR, the late payment fee, and what happens if you miss a payment. A trustworthy lender will not rush you through this.

07

Funds typically arrive within 24 hours. Several lenders offer same-day deposit when verification is completed early in the day. Confirm the lender’s timeline upfront if speed is the priority.

Red Flags to Watch For

Lenders who target people in financial hardship know the urgency is real and use it. When you are looking for emergency loans for single moms with bad credit, these warning signs can protect you from turning a tough month into something much worse. Check every lender against this list before you apply:

- APRs in the triple digits. Rates above 300% are legal in many states and can trap you in a debt cycle fast. Always verify the full APR before you sign anything.

- Automatic loan rollovers. A lender that rolls your unpaid balance into a new loan with added fees just keeps compounding your debt with no clear exit.

- Fees charged before funding. No legitimate lender asks for payment before you receive your money. This is almost always a scam.

- No state license on the website. Verify the lender is properly licensed in your state before sharing any personal or banking information.

- Pressure to sign immediately. A reputable lender gives you time to review the terms. If you feel rushed at any point, walk away.

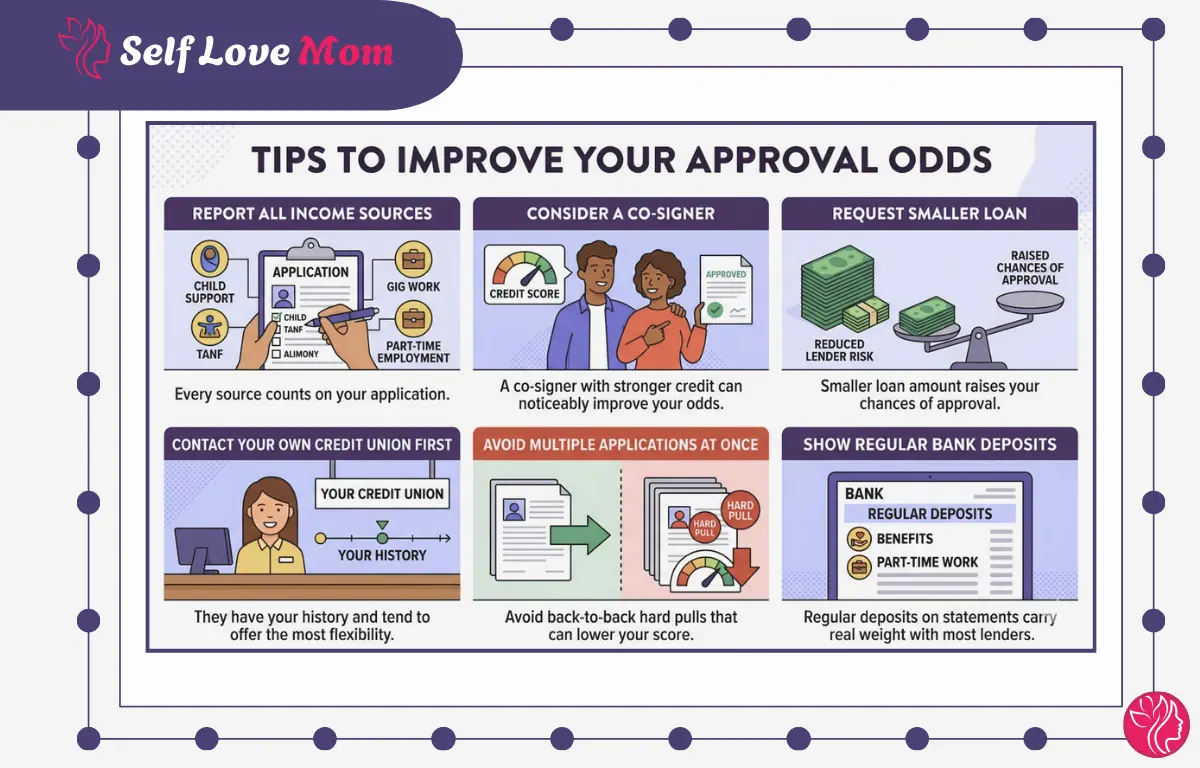

Tips to Improve Your Approval Odds

A lower credit score limits some options, but not all of them. These steps can genuinely improve your chances when applying for loans for single unemployed mothers or any type of emergency funding:

- Report every income source on your application. Child support, TANF, alimony, gig work, and part-time pay all count

- A co-signer with stronger credit can noticeably improve your odds if someone trustworthy is available and willing

- Requesting a smaller loan amount reduces the lender’s risk and raises your chances of approval

- Your own credit union is worth contacting first, since they have your history and tend to offer the most flexibility

- Avoid submitting multiple applications at once since back-to-back hard pulls in a short window can temporarily lower your score

- Bank statements showing regular deposits, even from benefits or part-time work, carry real weight with most lenders

How to Rebuild Credit After Using Emergency Loans for Single Moms

Paying back a loan on time is one of the best things you can do for your credit going forward. Every on-time payment gets reported, and those marks add up faster than most people realize. Here is how to make each one count:

- Pay on time every month. Payment history accounts for 35% of your score, the single most significant factor

- Set up autopay so a missed due date is never a possibility

- Keep credit card balances under 30% of your available limit to maintain a healthy utilization ratio

- Pull your free annual report at AnnualCreditReport.com and dispute any inaccuracies you find

- Setting aside even $10 to $20 a week builds a cushion that reduces how often you need to borrow. Our free single mom budget planner can help

- An emergency loan repaid on time can open access to better rates the next time you need support

Ready to Find the Right Emergency Loan for Your Situation?

Emergency loans for single moms are available right now, even with bad credit. Start by checking your options without affecting your credit score. Many lenders offer soft pull prequalification so you can compare rates and terms before committing to anything.

FAQs on Emergency Loans for Single Moms

1Can I get emergency loans for single moms with no job?

Yes. Child support, TANF, unemployment benefits, disability payments, and freelance income all count as income with many lenders. List every consistent income source on your application, regardless of whether it comes from a traditional employer.

2How fast can I get emergency cash as a single mom?

Many online lenders deposit funds within 24 hours of approval, sometimes the same day if verification is completed early. Nonprofit and government programs take a bit longer, but they often require no repayment at all, which makes the wait worth considering.

3What is the easiest emergency loan for single mothers to qualify for?

Payday alternative loans through credit unions and small personal loans through CDFIs tend to have the most accessible requirements for emergency loans for single moms. Both are solid first options for single moms who need funds quickly and have limited or damaged credit.

4Will applying for an emergency loan affect my credit score?

Prequalification uses a soft pull with no impact on your score. Once you accept a loan, repayment activity is reported to the credit bureaus. Consistent on-time payments can actively improve your score over the life of the loan.

5Are there grants instead of emergency loans for single moms?

Yes, and you should always check these before borrowing. Nonprofits, churches, community organizations, and government programs all offer grants with no repayment required. Visit Benefits.gov and 211.org to find what is available in your area.

Sources

- U.S. Census Bureau — Single Mother Households and Poverty Statistics

- Consumer Financial Protection Bureau — What to Know Before You Borrow

- National Credit Union Administration — Payday Alternative Loans Overview

- Benefits.gov — Financial Assistance Programs for Families

- AnnualCreditReport.com — Free Credit Reports for Consumers

- U.S. Department of Health and Human Services — TANF Program Overview