Quick Summary

- Loans for single moms with bad credit exist through federal programs, credit unions, CDFIs, and online lenders

- FHA home loans accept credit scores starting at 500 with a 10% down payment

- Federal student loans require no credit check and no cosigner

- Credit union Payday Alternative Loans are federally capped at 28% APR

- Always verify a lender’s state license before sharing any personal information

Bad credit doesn’t mean no options. It means knowing which options actually apply to your situation. In 2026, single mothers with lower scores have more paths available than most people searching for help ever find out — through federal programs, nonprofit lenders, credit unions, and online platforms built for borrowers the big banks turn away.

This guide breaks down loans for single moms with bad credit, the real costs, the lenders worth calling, what documents to bring, and the red flags that cost people thousands every year.

Understanding Bad Credit and Why It Affects Single Moms

A FICO score below 580 is classified as bad credit. For single mothers, this typically results from circumstances such as divorce, medical debt, job disruption, or childcare costs of $1,000 to $2,500 per month, not carelessness. A score in the 400s still qualifies for federal student loans, USDA housing programs, CDFIs, and credit union products.

Common reasons single moms have lower credit scores:

- Joint debts unpaid following a divorce or separation

- Medical bills were sent to collections before the first statement arrived

- Job loss or income reduction triggers a chain of late payments

- Childcare costs exhaust income before debt repayment

- Credit history is lost when shared accounts are closed after separation

- Deferred student loans are pulling scores down without any warning

Credit Score Ranges and What They Mean for You

| Credit Score | Rating | What It Means |

|---|---|---|

| 800 – 850 | Exceptional | Best rates, easiest approvals |

| 740 – 799 | Very Good | Near-best rates, most lenders approve |

| 670 – 739 | Good | Average rates, most loan products available |

| 580 – 669 | Fair | Higher rates, FHA loans available |

| 500 – 579 | Poor | Limited options, FHA with 10% down possible |

| 300 – 499 | Bad | Specialist lenders, CDFIs, and no credit check options |

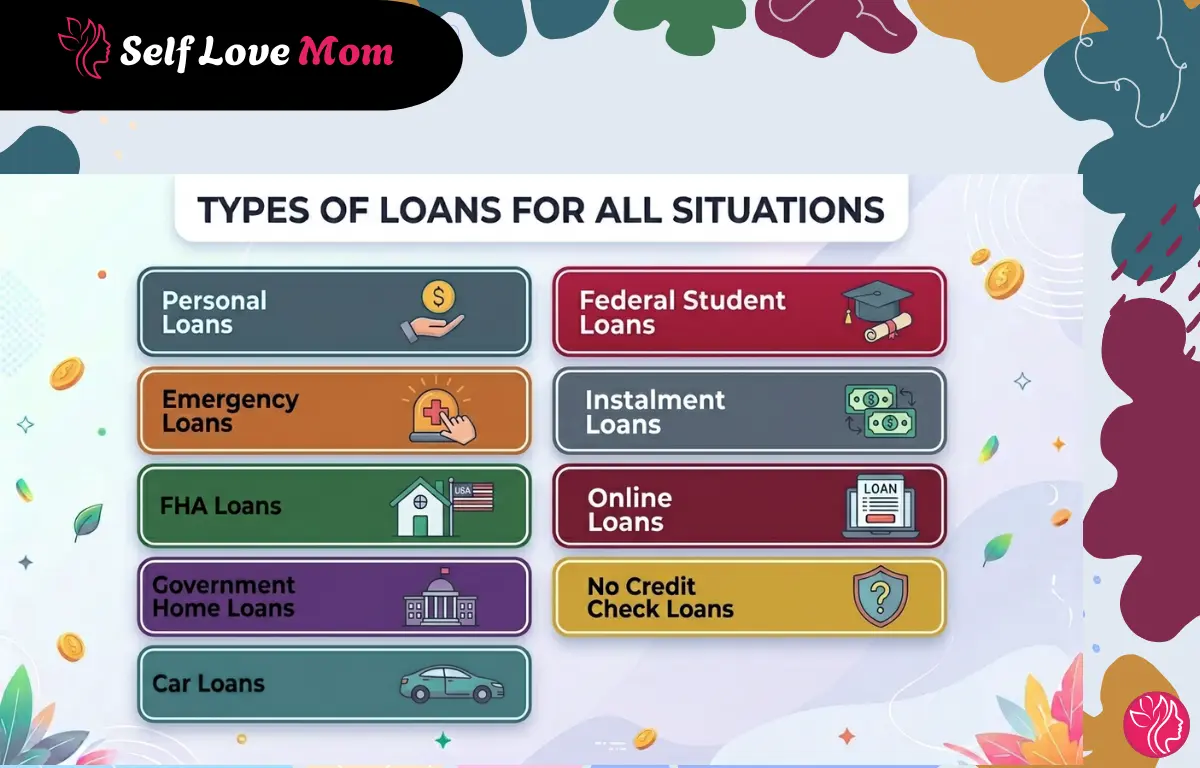

Types of Loans for Single Moms with Bad Credit

| Loan Type | Min. Credit Score | Typical Amount | APR Range | Best For |

|---|---|---|---|---|

| Personal Loans | 560+ | $500 – $50,000 | 6% – 36% | Bills, consolidation, any expense |

| Emergency Loans | None to low | $100 – $5,000 | 0% (nonprofit) to high | Urgent rent, utilities, medical |

| Installment Loans | 580+ | $1,000 – $25,000 | 9% – 35% | Fixed predictable payments |

| Online Loans | Varies | $100 – $35,000 | 6% – 99%+ | Fast funding, flexible requirements |

| FHA Home Loans | 500+ | Varies | Competitive fixed | Buying a home with a low down payment |

| Car Loans | 500+ | $5,000 – $40,000 | 7% – 29% | Reliable transportation |

| Federal Student Loans | No check | Up to $20,500/yr | Fixed gov. rate | College or trade school |

| CDFI / Nonprofit Loans | None to low | $500 – $50,000 | Below market | Flexible underwriting |

| No Credit Check Loans | None | $100 – $5,000 | Very high | Last resort only |

Detailed Breakdown of Loans for Single Moms with Bad Credit

1. Personal Loans for Single Moms with Bad Credit

Of everything on this list, personal loans for single moms with bad credit give you the most freedom. You can spend the money on anything — rent, a car repair, a medical bill, or childcare debt piled onto a credit card. No one asks what it’s for. Most online lenders now handle everything digitally, with same-day decisions and funds hitting your account within a day or two of approval.

- Best lenders: Upstart, LendingClub, Avant, OppLoans

- Loan amounts: $500 – $50,000 | Terms: 12 – 60 months

- Watch for origination fees of 1% to 8% taken out before funds reach you

- Adding a cosigner with good credit can bring the rate down significantly

2. Emergency Loans for Single Moms with Bad Credit

When the electric bill is overdue, or the car won’t start before your shift, you need money today — not next week. Emergency loans for single moms with bad credit are built exactly for that. Many funds within 24 hours. The safest option here is a credit union PAL loan, which is federally capped at 28% APR. That’s a completely different world from payday loans running above 300%. Find your nearest credit union here and call them first before going anywhere else.

3. FHA and Government Home Loans for Single Moms with Bad Credit

Most single moms in this situation assume homeownership is not available. For many, it isn’t. Federal programs were designed specifically for buyers with limited credit and limited down payment savings. FHA, USDA, and VA each work differently, and a HUD-approved housing counselor can help you figure out which one fits — for free.

- FHA loans: Min. 580 for 3.5% down, or 500 with 10% down — HUD.gov

- USDA loans: Zero down payment for qualifying properties — check eligibility

- VA loans: No minimum credit score set by the VA

- State HFA programs: Additional down payment help available in most states

4. Car Loans for Single Moms with Bad Credit

Getting to work and getting kids to school isn’t a luxury — it’s necessary. Car loans for single moms with bad credit are still within reach for those with a score below 600 because the vehicle backs the loan, which lowers the lender’s risk. Subprime auto lenders work with this situation every day. After 12 straight on-time payments, refinancing to a lower rate is usually on the table.

- Subprime specialists: Capital One Auto, DriveTime, Credit Acceptance

- APR range: 10% – 25% for bad credit vs. 5% – 7% for excellent credit

- A 10% down payment improves approval odds and cuts total interest paid

5. Federal Student Loans for Single Moms with Bad Credit

No credit check. No cosigner needed. Federal student loans for single moms with bad credit are the most open borrowing option available to anyone, regardless of score. Apply through FAFSA at studentaid.gov. If your income is low enough, Income-Driven Repayment can bring your monthly payment all the way down to zero.

- Pell Grants: Need-based aid that never has to be paid back

- Income-Driven Repayment: Monthly payments tied to your actual income level

- Private loans: Available through banks and credit unions, usually need a cosigner

- Many states offer extra scholarships specifically for single parents

6. Instalment Loans for Single Moms with Bad Credit

In these loans, you borrow a set amount and pay it back in equal monthly payments over a fixed period. No surprise balloon payment waiting at the end. No rollover trap. What makes these worth a serious look is that every on-time payment goes on your credit report, so you’re paying off debt and building your score at the same time.

- Good lenders: OppLoans, NetCredit, Mariner Finance

- Terms: $1,000 – $25,000 over 6 – 60 months

7. Online Loans for Single Moms with Bad Credit

The whole application takes under 10 minutes on your phone, you get a decision within hours, and the money lands in your account in a day or two. Comparison platforms like LendingTree, CashUSA, and PersonalLoans.com pull offers from multiple lenders through one soft inquiry, so your score never takes a hit. Before entering any personal information, check that the lender holds a valid state license.

8. Loans for Unemployed Single Moms

No W-2 doesn’t automatically mean no loan. CDFIs and nonprofits look at the whole financial picture, not just your employer. Child support counts. Alimony counts. Social Security, disability, unemployment benefits, and documented freelance income all count. Accion Opportunity Fund is a strong choice for self-employment and small business lending. TANF, WIC, and SNAP help reduce the immediate pressure while you work through your options.

9. No Credit Check Loans — Last Resort Only

These skip the credit pull and approve based on income. Cash advance apps like Earnin, Dave, and Brigit are the safer end of this — small amounts, no interest, nothing that will trap you. Payday loans above 300% APR are a completely different story. They’re designed to make full repayment nearly impossible, which keeps borrowers stuck in rollover cycles.

- Better option: Credit union PAL loans — no credit history needed, APR capped at 28%

What You Will Need to Apply

1. Personal, Emergency, and Instalment Loans

- Government-issued photo ID

- Social Security number

- Proof of address dated within the last 60 days

- Proof of income: pay stubs, bank statements, or benefit award letters

- Bank account and routing number for direct deposit

2. Home and Mortgage Loans

- Two years of tax returns and W-2 forms

- 30 days of pay stubs and 2–3 months of bank statements

- Documentation of other income: child support order, alimony, or disability letter

- Current lease or rental payment history

3. Car Loans

- Photo ID and proof of current address

- Proof of income and current auto insurance

- Down payment funds, if available

4. Federal Student Loans

- Social Security number and FSA ID from studentaid.gov

- Most recent tax return

- School enrollment confirmation and cost of attendance estimate

How to Apply for Loans for Single Moms with Bad Credit

Here’s how to get through the process of loans for single moms with bad credit without making costly mistakes:

- 1

Research: Pull your credit report at AnnualCreditReport.com, match your score to the right loan type using the table above, and use soft-pull prequalification tools to compare lenders without touching your credit.

- 2

Prepare: Get your photo ID, proof of income, and proof of address together before you start any application. If a cosigner or collateral is an option for you, decide that before you submit.

- 3

Apply: Submit your application, upload everything as PDFs, and check that the lender is state-licensed before sharing any personal details. Two minutes on your state regulator’s site can prevent a major problem.

- 4

Receive: Most loans for single moms with bad credit are funded in 1–2 business days. Read the full APR and repayment schedule carefully before spending anything, and set up automatic payments right away to protect your credit going forward.

Important Factors to Consider Before Taking a Loan

Before you sign anything, these are the five factors that matter most — and the ones most borrowers overlook until it is too late.

- 1

Check the full APR, not just the monthly payment: A low monthly figure can hide a very expensive loan. Always ask for the total repayment amount in writing so you know exactly what the loan costs from start to finish.

- 2

Watch for origination fees and prepayment penalties: Many lenders deduct 1%–8% from your loan before it reaches your account. Others charge a fee if you pay early. Confirm both upfront so there are no surprises.

- 3

Know how it affects your benefits: A lump-sum deposit may temporarily count as income or assets under SNAP, TANF, or Medicaid rules. If you receive means-tested benefits, speak to your caseworker before borrowing.

- 4

Keep your debt-to-income ratio in check: Lenders want total monthly debt payments below 43% of your gross income. Pushing past that threshold makes future borrowing — especially a mortgage — significantly harder.

- 5

Consider grants and assistance programs first: Local nonprofits, community action agencies, and state emergency funds sometimes cover rent, utilities, and car repairs with money you never have to repay. Exhaust those options before taking on debt.

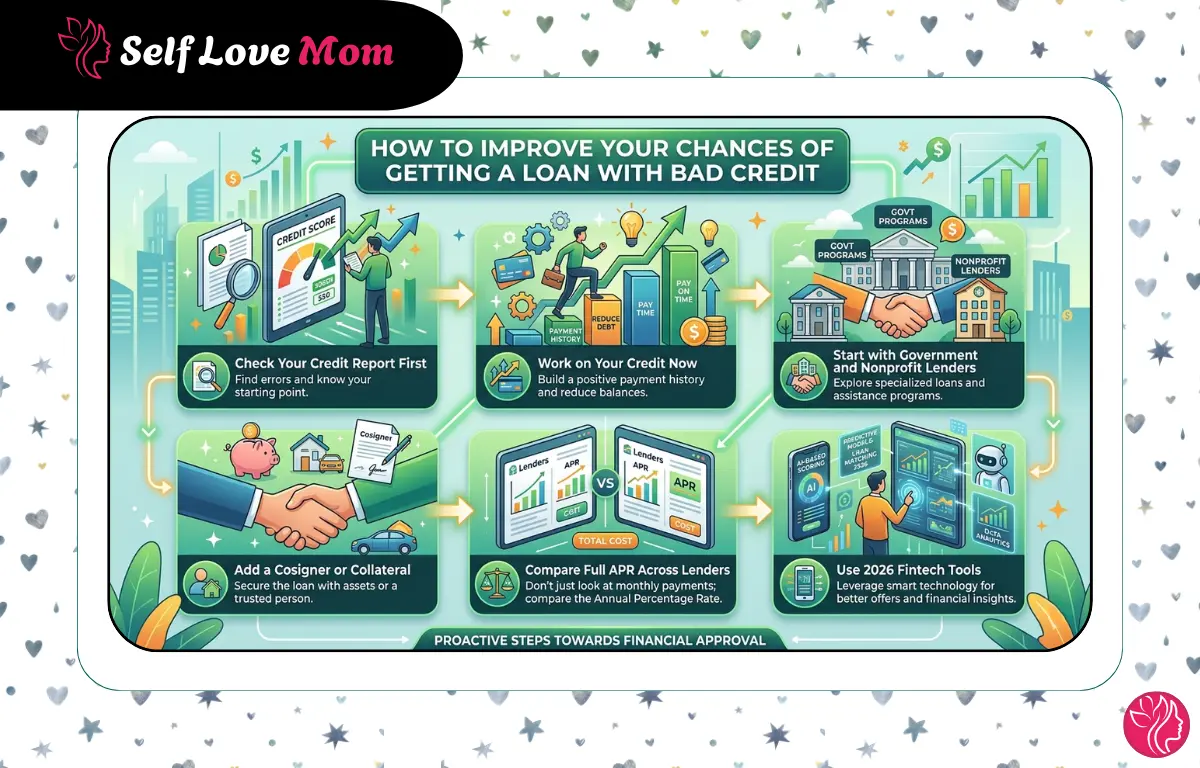

How to Improve Your Chances of Getting a Loan with Bad Credit

A few things done before you apply can move the needle on both approval odds and the rate you end up with:

- Check Your Credit Report First: Get free reports at AnnualCreditReport.com. One disputed, inaccurate collection account can raise your score 20 to 40 points before you apply anywhere.

- Work on Your Credit Now: Open a secured credit card, use it for small purchases, and pay the full balance every month. Six months of this consistently shifts where your score lands.

- Add a Cosigner or Collateral: A cosigner with good credit opens up better loan options. A paid-off vehicle or a savings account as collateral can get you improved terms at credit unions and banks.

- Compare Full APR Across Lenders: Soft-pull tools let you see real offers from multiple lenders without affecting your score. Compare total repayment cost, not just the monthly payment number.

- Use 2026 Fintech Tools: Many lenders now look at actual cash flow through open banking rather than relying only on the credit score. Platforms like Possible Finance and Creditspring can help borrowers whose scores don’t reflect their current income reality.

Red Flags and Warning Signs to Avoid

Predatory lenders target people in urgent situations. Know what to look for before you share anything with anyone:

- Guaranteed Approval Before Any Application — No real lender approves without reviewing your file first. Any guaranteed approval claim is either a scam or a setup for fees you won’t see until it’s too late.

- Upfront Fees Before You Receive Funds — Legitimate lenders never ask for payment before funding. Wire transfers, gift cards, or crypto requested before you see any money is always a scam — no exceptions.

- No Verifiable State License — Check the lender’s license on your state regulator’s site and verify at bbb.org. No license means no accountability if something goes wrong.

- Pressure to Sign Immediately — Repeated calls, expiring offers, and urgency tactics are deliberate manipulations. Real lenders give you time to read everything before signing.

- APRs Above 36% in Fine Print — Always ask for the full APR in writing. Above 36% is high-cost, above 100% is extreme risk, and above 400% is predatory.

- Incomplete or Verbal-Only Documentation — Never sign anything with blank fields or agree to verbal terms alone. Every legitimate lender puts the full agreement in writing before you sign.

- Requests for Sensitive Info Too Early — No lender needs your bank login or SSN before a formal application is in place. Handing it over too early is a direct path to identity theft.

Your Credit Score Is Not Your Whole Story

Thousands of single mothers have worked through exactly this situation — found a loan, paid it off on time, and come out with stronger credit and a financial foundation that actually holds. The right lender is out there for you. Pull your free credit report first, fix any errors, and reach out to a credit union or CDFI before going anywhere else.

FAQs on Loans for Single Moms with Bad Credit

Can I get a loan as a single mom with bad credit?

Yes — more loans for single moms with bad credit exist than most search results show. Credit unions, CDFIs, online lenders, and nonprofits all work with single moms who have bad credit. FHA home loans start at a 500 score, and federal student loans skip the credit check entirely.

What credit score do I need for loans for single moms with bad credit?

FHA home loans accept scores from 500. Most online personal loan lenders start around 560. Federal student loans through FAFSA have no credit requirement at all.

What is the easiest loan to get with bad credit?

Federal student loans are the easiest to get for single moms with bad credit — no credit check, no cosigner needed. For other purposes, personal loans and instalment loans through credit unions are generally the most accessible when your score is under 600.

What if I am unemployed? Can I still qualify?

Often, yes. Child support, alimony, disability, and documented gig income all count toward qualification at many CDFIs and nonprofits. TANF and SNAP also ease the immediate financial pressure while you sort through your options.

How do I recognise a loan scam?

Upfront fees before you receive money, guaranteed approval before any review, pressure to sign right now, and no verifiable state license are all red flags. Check every lender on your state regulator’s website before sharing anything personal.